“Taxation Without Representation.”

Three words that led to the American Revolution.

And today, in crypto, we’re living them again.

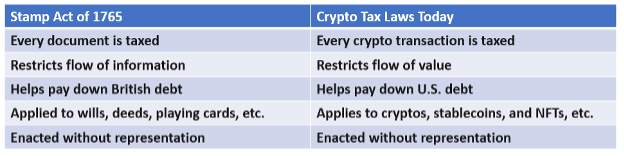

In the 1700s, the British government began to levy a series of increasingly unpopular taxes on the fledgling American colonies, as Britain was mired in debt from the messy Seven Years’ War. Among the worst of these taxes was the Stamp Act of 1765, which put a tax not on stamps, but on all paper documents produced in the colonies.

Think about that. As an early American settler, it was hard to find broadband, so paper documents were your primary source of information. Now the government required an official “stamp” on every document that came from the printer, showing the tax had been paid. (Thus, the “Stamp” Act.)

Taxing the flow of information is a terrible move. Not only does it restrict the free flow of ideas (which is how healthy economies grow), but it makes everyone angry – especially when they have no say in how the law got passed in the first place. (Thus, “taxation without representation.”)

Today, this would be like a tax paid on every web page that we download, or every email that we send.

Or perhaps, a tax paid every time we buy and sell a crypto asset.

Which is exactly the position we find ourselves in today: crypto taxation without representation.

How Crypto Taxes Work

Bankless recently put together an excellent year-end Crypto Tax Planning Guide for the U.S., which I will summarize in a few bullet points:

- If you bought and sold crypto, it’s a taxable event.

- If you traded crypto, it’s a taxable event.

- If you bought and sold NFTs, it’s a taxable event.

- If you traded NFTs, it’s a taxable event.

- If you made a DeFi loan, earned “interest” in the form of protocol tokens like cETH, then swapped those back into ETH, it’s likely a taxable event. (The IRS is still figuring out how to tax this one.)

In short, every time you swap one digital asset into another, or a digital asset back into USD, it’s a taxable event.

Let’s see how this tax situation compares with the Stamp Act of 1765.

As the Stamp Act choked the free flow of information (making it more expensive to publish), our crypto tax laws choke the free flow of value (making it more expensive to build and innovate on this new technology).

On one hand, governments refuse to acknowledge the “value” of these new digital assets.

On the other hand, governments have no problem collecting taxes on this value.

You can’t have it both ways.

You can’t say that bitcoin is dangerous and DeFi is shady, then legitimize their use by taxing Every. Single. Transaction.

Yellen, Warren, and all the rest: you can’t have it both ways.

Either we acknowledge the inherent value of crypto assets, and make a place for them in the current financial system … OR we completely overhaul our approach to crypto taxes.

Otherwise, we have no one who truly understands crypto helping make these laws. It’s TAXATION WITHOUT REPRESENTATION.

This is How Governments Smother Money

Let’s fast forward in history to the 1800s. America is now an independent nation, thriving and prosperous. The new financial challenge is from within, as “wildcat banks” begin to spring up across the American frontier, printing their own money.

This time period is a great analogy to what’s happening right now in crypto. Before the days of national banking, local banks would print their own private money, which you could use to make local purchases. (Just like minting your own crypto token.)

The problem was that some of these banks were manufacturing the money out of thin air (just like most crypto tokens today). Your local wildcat dollar might not be accepted in the next state (just like most crypto tokens don’t have enough liquidity to sell them back).

The creation of the National Bank Acts of 1863 and 1864 solved these problems by creating a national banking system and, importantly, issuing a 10% tax on state banknotes. This meant that your “wildcat dollar” was now only worth a considerably-less-wild 90 cents.

Imposing a tax on unwanted forms of money is the easiest way for governments to smother them.

This is the reason we constantly preach long-term holding of your digital assets: otherwise you’re being eaten alive with fees (on the blockchain side) and taxes (on the government side).

Every tutorial, every YouTube video, every “crypto newbie guide” ignores this basic fact. Every time you sell your crypto for profit, even swapping into another crypto, it’s a taxable event.

And when the government is still struggling to understand bitcoin, but still taxes it, it’s fair to say we have taxation without representation.

Crypto Taxes: The Way Forward

Last night we hosted Chris Giancarlo, the former chairman of the CFTC and one of the most forward-thinking government officials on crypto regulation. (His new book CryptoDad is terrific: put it on your holiday wish list.)

In our networking session after the event, Chris laid out his predictions for what will happen next. He pointed out that 2022 will be an election year, so no great strides are likely to be made in regulation. However, 2023 is likely to be a turning point.

He said major crypto players are beginning to make large political donations, like the $5 million Sam Bankman-Fried donated across the political spectrum. “Money,” Chris said, “is like mother’s milk for Congress.”

I agree with Chris: we are likely to see meaningful change in U.S. crypto regulation and tax laws, but not until 2023. (That’s tomorrow in crypto time.)

Fortunately, trade groups like the Chamber of Digital Commerce have been recommending smart legislation for years. Here are a few great suggestions from their Legislator’s Toolkit:

- Limit and standardize tax obligations. To encourage digital e-commerce, we have to treat cryptocurrencies as currencies: we shouldn’t be taxed twice for using crypto to buy coffee.

- Promote blockchain innovation through tax credits. For example, our Make America Green Again idea would encourage bitcoin miners to build out our solar infrastructure by giving them tax credits for mining with 100% renewable energy.

- Accept crypto to pay taxes. Here’s a twist: allow citizens to use crypto to pay taxes, as well as other government services (drivers’ licenses, registrations, etc.).

Summing Up:

- Today’s crypto tax laws are like the Stamp Act of 1765: they restrict the free flow of information (i.e., digital value), as well as being “taxation without representation.”

- The lessons of “wildcat banks” in the 1800s is that a strong national bank can co-exist with healthy regional banks, but smart legislation is needed (like the National Bank Acts).

- The frameworks for this legislation already exist (see the Legislator’s Toolkit), and we can expect these to really take root in 2023, as more crypto millionaires begin donating to politicians.

Evolution, Not Revolution

It’s hard to be patient. But we’ve always preached “evolution, not revolution.” Good things take time.

Keep patiently investing, selling only when necessary.

Keep up the pressure by emailing your Senator or elected official.

And keep paying your taxes.