Jack Bogle, the founder of Vanguard Investments, was a titan of investing — but he wasn’t your typical wolf of Wall Street.

Born in 1929, the Depression instilled in Bogle a deep respect for saving. He was skeptical about the high fees charged by investment managers and banks, which silently ate away the returns they were supposed to be generating for their clients and customers.

He founded Vanguard, which became an industry giant by prioritizing investor returns over company profits. Vanguard also launched the first low-cost index fund for everyday investors, democratizing investing for the people. (It’s the same fund we use in our Blockchain Believers Portfolio.)

He founded Vanguard, which became an industry giant by prioritizing investor returns over company profits. Vanguard also launched the first low-cost index fund for everyday investors, democratizing investing for the people. (It’s the same fund we use in our Blockchain Believers Portfolio.)

Throughout his long career, Bogle challenged the industry’s focus on beating the market, crusading for long-term, low-cost investing. The guy was obsessed with fees.

Bogle died in 2019, at the age of 89 (read more about his remarkable life here). And today, we could really use him for crypto, which is absolutely loaded with fees.

Crypto Fees, Explained

Even though crypto was founded with the idea that we could send money around the world, instantly, with no fees, the opposite is true: using crypto is usually way more expensive than TradFi for ordinary users.

- Exchange Fees: You’ll pay fees for buying and selling crypto on an exchange platform, either a flat fee or a percentage of the transaction. You may also pay “hidden” fees in maker-taker fees and spread fees. You also may pay fees to move money into or out of your account!

- Network Fees: You’ll pay “gas fees” to process transactions on most blockchains. These fees are paid to miners or validators who run the network. These fees can get outrageously expensive during peak times, especially for small transactions.

- Wallet Fees: Some wallets, such as custodial wallets, might even charge fees for sending and receiving crypto.

- Taxes: When you sell crypto for a profit, you owe capital gains taxes on the difference between your purchase price and selling price. Tax rules can vary depending on where you live and how long you held the crypto, but if you made a profit, you’re paying tax (up to 34% in the U.S.).

It helps to visualize this. Let’s say you bought some bitcoin last month, made a $1,000 profit, and want to cash out. Here’s what you’d pay in taxes and fees:

It gets even worse if you only made a $100 profit:

Over a quarter of your profits, down the drain. Imagine all the short-term investors who are doing this kind of trade all the time.

There’s a better way.

Fee vs. Free

The only transaction that’s free is just handing cash from one person to another.

Even then, you may have paid fees to get money out of the ATM (average fee is around $4 or $5, according to Bankrate). You may have also paid monthly fees to the bank (average $15 on an interest-bearing checking account).

Everything else takes fees. Credit cards. Stripe. PayPal. Wire transfers. Either you’re paying a fee, or the merchant is paying a fee. For most transactions it’s around 3%, or sometimes a flat fee (around $25 for wire transfers, according to NerdWallet).

The people who have it worst are those without a lot of money. Banks will waive fees for larger customers, but the minimum amount to avoid fees has soared to over $8,600 on average. And for those who occasionally withdraw more money than they have in the account, they pay a whopping $27 each time they overdraft.

It’s easy to see this system as another way that the rich get richer, while the poor get poorer. If you have money, the system is free. If you don’t, the system is fees. Free vs. Fee.

Blockchain is supposed to solve all this, right?

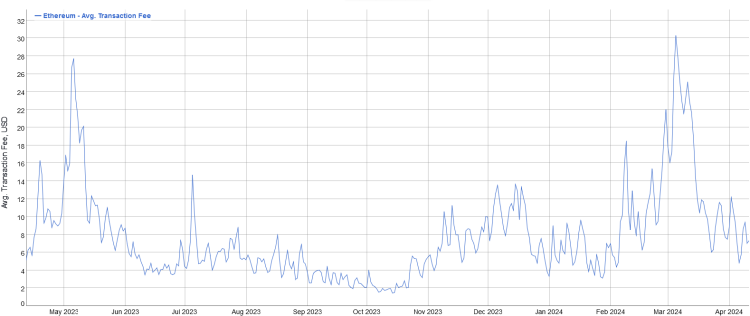

Average Fees on Ethereum

The average fee for an Ethereum transaction – the Layer-1 blockchain where all the action is happening – is about $6.50. And on any given day, it can shoot up as high as $30!

What’s worse, Ethereum fees are not proportional to the amount transferred. With a bank ATM, you generally pay the same service fee, regardless of how much money you withdraw. With Ethereum, fees are charged on the complexity of the transaction, which is much harder to predict.

What's even worser: the fee is more expensive when the Ethereum network gets congested – which is exactly when most people want to buy and sell, because they’re fueled by FOMO.

The outrageous fees in crypto are a huge, gaping flaw for those of us trying to build long-term wealth. A bank would never be able to legally charge you 30% in fees. (Unless of course you are poor. Then they can overdraft away.)

Of course, there are alternative blockchains with lower fees than Ethereum (like Solana). And there are Layer-2 platforms that let you do Ethereum transactions more cheaply (like Arbitrum).

But because Ethereum is where the action is (DeFi, NFTs, and all the other cool stuff), Ethereum is where the problem is.

Fees are the huge, unspoken secret of crypto. Developers, miners, Vitalik: you’ve got to do better.

In our quest to beat the banks, we’ve got a long way to go.

Taxes: The Biggest Fee of All

Fees are another reason we focus on long-term investing: every time you swap one token for another, every time you move money in or out of crypto, you’re paying these outrageous fees.

But there’s another reason to hold for the long term: every time you make a transaction, it’s a taxable event.

This means if you made money, you’re paying taxes on the gain: in the U.S., it’s 15-20 percent for most people. Think of this as a government fee.

But the cost to hold your crypto, and let it grow, is zero. Nothing. Nada. Once you’ve bought your crypto, it’s completely free to hold it.

To summarize: Once you’ve bought crypto investments, avoid moving them. It’s tempting because it’s so easy: all you have to do is click the “Swap” button in your Metamask wallet. Avoid this temptation.

Even when the market is going nuts, with everyone buying or selling, we keep calm and HODL on.

Investor Takeaway

Jack Bogle constantly argued on behalf of investors, whose profits could be eaten away over a lifetime by financial institutions that constantly nibbled away fees.

We not only follow Bogle’s philosophy, we use his funds.

To repeat our strategy: We set up a steady-drip withdrawal from our bank account each month, invest it in a Vanguard all-stock fund, a Vanguard all-bond fund, and a little bit of crypto (no more than 10% of your total portfolio.) More on our investing approach here.

Even though blockchain fees are unreasonable today, it does not mean we stay away from crypto completely, as the potential profits are too great. It does mean, though, that we avoid moving money until the developers finally get this fixed.

If we can make smart blockchain investments, and leave them alone, we can build wealth faster. When there are no transactions, there are no transaction fees. That means your growth is free, and you're free to grow.

Free, not fee.